LeadSpace rolled out its Customer Data Platform (CPD) fall release with improved processing of first-party data, enhancements to their Salesforce app, and refinements to their Ideal Customer Profile (ICP) modeling. Automated ingestion of first-party data and custom data sources deliver unified customer profiles “for use across systems.” Automated data onboarding assists with AI modeling, scoring and analytics, and enterprise software activation.

“Customers

can use data on engagement, product use, relationship, and other information

unique to their business to power real-time orchestration of activities and

processes,” stated the firm. “Decisions about how to route leads, assign

nurture programs, segment for campaigns, and personalize interactions can now

be made with all the intelligence of the CDP and a complete customer view.”

The fall release also supports data hygiene with the sunsetting of Data.com Clean in mid-2020. Both real-time and on-demand matching and enrichment are supported. Triggers automatically identify new or updated records and automatically look to match them against the LeadSpace CDP. At the end of the year, a sync button will be displayed within individual records.

“Getting a complete view of the customer is critical to improving the customer experience for B2B. Buyers no longer tolerate generic and impersonal content and interactions. Our Customer Data Platform gives B2B marketers a real path to being able to orchestrate the ideal customer experience at scale. Improving the ability to ingest 1st party data makes that even more powerful because it is unique to each of our client’s journey with their customers.”

LeadSpace CEO Doug Bewsher

Enhanced

ICP Analytics help select the right accounts and personas for ABM targeting.

Interactive, filterable reports display account, contact, and intent data

matched against conversion and revenue data to “uncover which categories and

segments have performed well historically.”

LeadSpace On-Demand look-a-like segment building now supports company suppression.

LeadSpace customers include Microsoft, HPE, SAP, Iron Mountain, IBM, and Symantec.

InsideView launched its new Data Integrity service for Salesforce. Data Integrity is a customer data management solution that provides data visualizations, ongoing data hygiene maintenance, and data health analysis for CRMs. According to the firm, the service is fully integrated with Salesforce and “offers an easy migration path for customers using Data.com.”

“Data is the world’s most valuable resource—it’s the new fuel. Maintaining the quality of that resource should be paramount for every company. InsideView Data Integrity was created to help companies get the most out of their data by maintaining an accurate and rich customer database, and check on the health of that data at a glance.”

InsideView CEO Umberto Milletti

Salesforce

admins control which records are managed, which fields updated, and the

frequency of updates. Along with historical match and update trend

graphs, they can review a data hygiene dashboard that displays the number of

family tree linkages, duplicates, past employments, lead-to-account mapping,

etc.

Data

Integrity features include

Account, Contact, and Lead “stare and compare” updates

Separate Match Score thresholds for accounts, contacts, and leads which allow for differing degrees of match accuracy based on the record type

An Update CRM button within the InsideView Sales product. Updates are subject to rules set by the Data Integrity account administrator.

Validation of business emails associated with leads and contacts

Dashboards for Accounts, Contacts, and Leads which provide segmentation analysis, duplicate and match rates, email counts, segment/team distribution, etc.

A Processes Dashboard which tracks Data Integrity processing and action items

B2B DaaS and

sales intelligence firms have been looking to take the lion’s share of

Salesforce’s Data.com business which is now being decommissioned. The

opportunity is likely around $250 million (legacy clients business plus

additional revenue from superior offerings). The Prospector and Clean

services are no longer sold, but final contracts are being fulfilled through

the middle of next year. InsideView offers both sales and data management

solutions as does Dun & Bradstreet, Zoominfo, and Infogroup.

Data Integrity Processes Dashboard

Clean data

is critical to a series of B2B data workflows including territory assignments,

account hierarchies (corporate linkage), lead-to-account management,

segmentation analysis, duplicate record prevention, and email validation. Accurate

and complete data is also critical for account planning and messaging, ICP /

TAM analysis (supported via InsideView’s sister product Apex), and reducing the

time spent by sales reps entering and maintaining company and contact data.

Data

Integrity pricing is tiered based on the number of CRM seats.

InsideView

covers 13.5 million global companies and 32 million contacts spanning eighty

fields. Account data includes standardized addresses, sizing variables,

and parent/subsidiary linkages.

The firm

recently expanded its AsiaPac company coverage in four countries: New Zealand

(25K total), Hong Kong (40K), India (150K), and Singapore (40K). Total

coverage for the region (Asia, Oceania, Middle East) is now at 840K companies.

The expanded coverage is derived from existing and new vendors along with

government registries.

Data

Integrity is currently available for the AppExchange with Microsoft Dynamics

365 queued up next. Other CRMs will follow.

B2B DaaS and contacts vendor DealSignal announced the availability of CRM Data Health, a Salesforce module that continuously refreshes, enriches, and reverifies lead, contact, and account records. DealSignal data is GDPR-compliant and based upon AI validation and human verification.

“Rather

than comparing dirty CRM data against other static data sources that may

themselves be outdated, DealSignal CRM Data Health takes a dynamic, on-demand

enrichment and verification approach that uses both AI and human intelligence

to ensure near-perfect accuracy,” stated the firm. “DealSignal CRM Data

Health delivers a reliable alternative for companies looking to replace

Data.com.”

Like other CRM hygiene apps, CRM Data Health includes a free data health audit. The CRM data enrichment includes detailed contact profiles, Bombora buyer intent, and firmographics. Along with CRM hygiene, customers can enrich inbound leads, events lists, and third-party lists.

“Bad CRM data is a pervasive issue that has a negative ripple effect on B2B marketing and sales performance: from inaccurate ABM targeting, to bounced emails that can damage sender reputation, to outdated or irrelevant contacts that clog marketing automation systems at a great cost,” said DealSignal founder & CEO, Rob Weedn. “Industry studies find that up to 50 percent of CRM data is incomplete, out-of-date, or inaccurate. Compounding the issue, data decays at a rate of over two percent per month, so maintaining data health is a constant challenge that requires an on-going solution—much like you can’t get in shape by going to the gym once. We’ve introduced DealSignal CRM Data Health to help Salesforce customers continuously maintain rich, accurate and verified target audience data, and keep it fresh on a regular schedule.”

With the decommissioning of Data.com, vendors like Dun & Bradstreet, InsideView, Zoominfo, and DealSignal are jumping into the fray. If you are looking to make your sales reps more effective, your segmentation more accurate, or your Einstein predictions more precise, then you should be evaluating a Lightning Data or general data quality solution for your CRM.

InsideView Append for Salesforce is a Lightning Data Solution for ongoing data enrichment and maintenance.

InsideView went on the offensive to capture Data.com customers as Prospector and Clean are phased out over the next year. InsideView is offering their free Data Health report “as many Data.com customers have seen a degradation of data quality since the announcement was first made over a year ago.”

Data.com Prospector and Clean contracts are no longer renewing beginning this month.

“Customers

tell us that the switch from Data.com to InsideView was not only easy but gave

them more confidence and made their data more useful than ever,” said Umberto

Milletti, CEO of InsideView. “Now we’re adding more data, more

technology, and more analytics to make InsideView even better, because it’s not

just about the data. It’s about how it helps drive marketing, sales, and

the bottom line.”

InsideView

covers twice as many contacts (35 million) as Data.com including global

contacts and emails. InsideView also emphasized its improved match logic:

Comprehensive analysis of customers’ data quality (i.e. malformed company names, transposed data fields, incomplete addresses, etc.)

Flexibility in match logic based on business needs and data availability (i.e. company name, website/email domains, street address, city, state, country, etc.)

Higher match rates and accuracy using probabilistic intent (e.g. inferring a match result based on geographic or industry clustering, etc.,) within the input file.

Clear explanations of why records match and suggestions for those that don’t match.

Other enhancements include expanded location data with site counts and “fine-grain control for selecting CRM records under management and field level update rules.”

The Top Five Lightning Data vendors (August 8, 2019)

In the Sales Intelligence category, the top four B2B sales intelligence AppExchange offerings come from Zoominfo, DiscoverOrg, D&B Hoovers, and InsideView.

InsideView also announced that its Microsoft Dynamics Insights service will be available at no charge through the end of current MS Dynamics 365 contracts. Current Insights customers simply need to opt-in. Companies that do not qualify can license Insights directly from InsideView.

“Microsoft is committed to delivering stellar customer experiences and it became clear to them, after announcing changes to their data augmentation strategy in January, that many customers love and value InsideView Insights,” said InsideView Senior Product Marketing Manager Janice Bowen. “In response to their needs, Microsoft decided to continue providing InsideView’s data and intelligence solution for an extended period of time.”

Oracle recently acquired DataFox, providing them with access to 2.8 million company profiles, including funding and M&A data. DataFox “gives customers real-time insight to know when a business exhibits noteworthy behaviors.”

“The combination of Oracle and DataFox will enhance Oracle Cloud Applications with an extensive set of trusted company-level data and signals, enabling customers to reach even better decisions and business outcomes,” wrote Oracle’s EVP of Applications Development Steve Miranda to customers and partners.

Oracle provides the following deal shorthand:

Oracle Cloud Applications + DataFox = Even Smarter Decisions

DataFox is growing its database at 1.2 million companies annually. The database will deliver real-time insights into its cloud-based ERP, CX, HCM and SCM platforms.

DataFox Data Engine Overview (Oracle Presentation, October 23, 2018)

In a bit of extreme puffery, Oracle described DataFox as the “the most current, precise and expansive set of company-level information and insightful data.” Bureau van Dijk and Dun & Bradstreet have 50X the active company coverage including detailed global linkage, risk models, and multi-year financial data. Bureau van Dijk also offers the Zephyr database, an M&A and funding dataset with over twenty years of closed, pending, and rumored deals. Where DataFox may have an advantage is in their focus on mid-size and emerging companies which have been recently funded, but this is a small subset of the company universe.

DataFox will continue to sell and support its products. However, the DataFox roadmap and product line are fluid:

“Oracle is currently reviewing the existing DataFox product roadmap and will be providing guidance to customers in accordance with Oracle’s standard product communication policies. Any resulting features and timing of release of such features as determined by Oracle’s review of DataFox’s product roadmap are at the sole discretion of Oracle. All product roadmap information, whether communicated by DataFox or by Oracle, does not represent a commitment to deliver any material, code, or functionality, and should not be relied upon in making purchasing decisions. It is intended for information purposes only, and may not be incorporated into any contract.”

Along with AI insights, Oracle called out the needs for quality data to back data maintenance, artificial intelligence, and business signals.

Customer Data Challenges (Oracle Presentation, October 23, 2018)

DataFox has over 275 customers including Goldman Sachs, Bain & Company, Outreach, Live Ramp, and Twilio.

DataFox raised $19 million in funding. Terms of the deal were not disclosed. In January 2017, DataFox was valued at $33 million by Pitchbook.

Oracle should study Salesforce’s acquisition of Jigsaw (later renamed Data.com) as a cautionary tale. Software companies struggle in selling data files as company and contact data decays rapidly and it is difficult to push data quality above 90% absent large editorial investments. Furthermore, Jigsaw never represented more than 1% of Salesforce revenue so quickly fell off of the company’s internal radar. The firm is now looking to decommission Data.com and asking its AppExchange partners to fill the sales intelligence and data hygiene gap left in its absence. Coincidentally, DataFox is one of Salesforce’s Lightning Data partners.

On the positive side, LinkedIn hit $1.3 billion last quarter and has thrived under Microsoft’s ownership. However, LinkedIn was a much more mature company at acquisition than DataFox with multiple revenue streams and a unique user generated content model. Microsoft has provided LinkedIn with development capital and allowed it to maintain its independence. It has also looked to leverage LinkedIn and Microsoft strengths when building sales and marketing products, instead of simply copying other vendors. For example, Sales Navigator continues to respect the privacy of its members while using aggregated data to provide hiring and employment insights that other companies cannot deliver. Navigator has also added strong messaging tools (chat, InMail, and PointDrive) which work around its lack of company emails. Other innovations include SNAP workflow connectors, its new Pipeline CRM updating tool, and Buyer’s Circle for identifying the buying committee at large firms.

North American Sales Intelligence Market Sizing Model (Excel)

The 2017 Market Size of North American Sales Intelligence Vendors. Includes vendor product features, market share, and notes. GZ Consulting Copyright 2018.

$750.00

For the past few years, I have been sizing the North American Sales Intelligence Market. This is the largest of the markets as Europe and AsiaPac are more fragmented (the UK is the only other mature market).

In 2017, I estimated the market at $950 million with LinkedIn Sales Navigator as the top vendor. While new firms continue to enter, the top four vendors earn two of every three dollars in the industry. The top four concentration increased 7% last year, mostly due to the acquisitions of Avention and RainKing.

The LinkedIn Market Share Section of the 2017 North American Sales Intelligence Market Sizing

The industry grew 17% over the past year with the majority of this growth being captured by LinkedIn Sales Navigator, DiscoverOrg, and Zoominfo. TechTarget, which was off my radar in 2016, has also seen rapid growth in 2017 and 2018.

DiscoverOrg acquired RainKing at the end of August 2017 so two-thirds of its revenue was recognized as RainKing and one-third as part of DiscoverOrg. Combined, the two firms earned around $118 million least year with DiscoverOrg ending the year with a $130 million plus ARR. DiscoverOrg raked in two of every three dollars within the technology sales intelligence sub-segment.

LinkedIn holds a nearly 30% market share. It has grown rapidly while remaining under the radar of its peers as it is often used as a complementary service to other sales and marketing intelligence services.

Data.com’s 2017 revenue was stable but Dun & Bradstreet forecasted a 30% drop in 2018 (D&B is a revenue share partner on the service). I anticipate that much of this revenue will shift to other vendors in 2018 and 2019. Dun & Bradstreet is in a strong position to take much of this share, but other vendors are pushing hard to acquire Data.com clients.

Zoominfo was ahead of the other sales intelligence vendors in recognizing the value of adding marketing functionality alongside their sales tools. This has put them in a strong position for data services. They also built the deepest set of global contacts with emails and direct dials and were early to build out connectors (CRM, MAP, Sales Engagement, and Chrome).

I am making my market model available for license (See PayPal button at top) as an Excel spreadsheet. It includes revenue numbers by company along with market share, key features, and notes.

SFDC is promoting Lighting Data solutions as an alternative to its Data.com Prospector and Clean offerings. Salesforce Lightning Data partners include Clearbit, HG Data, Bombora, MCH, DataFox, InsideView and Dun & Bradstreet. Additional partners are planned.

Salesforce told its Data.com Connect customers that the product will no longer be available as of May 4, 2019. As such, the firm will not renew any customers after May 3rd of this year, and users will not be able to license any points, contacts, or plans after May 3rd. However, users will be able to earn points through community updates through the expiration of the product. While Salesforce has not announced shutdown dates for the native Salesforce Data.com Clean and Prospector offerings, their shutdown is “currently targeted for some time in 2020.”

Data.com Connect contacts data will continue to “used in the maintenance of the Data.com Clean and Prospector products,” said the firm. “After the Data.com end-of-life is complete, the contact database may be archived by Salesforce.”

Data.com Connect is the successor to Jigsaw, which the firm acquired in 2010 for $142 million. Connect Members either purchased plans or earned points through adding and maintaining records within Connect. After acquiring the database, Salesforce realized that Jigsaw company data was too weak to be sold and partnered with D&B (now Dun & Bradstreet) to deliver the WorldBase company file alongside Jigsaw contacts. This partnership was in place until early 2017 when SFDC announced the end of the licensing relationship. Legacy customers continue to receive Data.com WorldBase account data, but the firm is encouraging clients to evaluate Lightning Data partnership offerings from Dun & Bradstreet, Bombora (intent), HG Data (technographics), DataFox, Clearbit, MCH (healthcare), and InsideView.

Future Lightning Data partners include Thomson Reuters, Aberdeen (technographics), Datanyze (technographics), Compass, and Equifax.

“We’ve built a powerful, flexible set of capabilities into the Salesforce platform we call the Lightning Data Engine. It uses sophisticated matching algorithms and machine learning to make it easy to implement and deliver strategic data and insights from trusted, third-party sources. Lightning Data apps give customers next-level data quality, enabling them to create more intelligent processes built on better, more targeted data, which improves CRM user adoption and ROI. Best of all, seamless integration requires minimal ongoing maintenance, and makes data readily available on any device without IT involvement.”

Salesforce.com

Dun & Bradstreet said that it expects Data.com revenues to decline 30% in 2018. The announcement that the Data.com Prospector and Clean products will be shuttered in 2020 is likely to expedite the revenue wind down.

I attended the Salesforce World Tour Event in Boston yesterday and came away a bit underwhelmed. I’ve attended it for the past four or five years, so that may be part of the reason I didn’t stay for the full day.

In attending, I had several topics top of mind:

What is the future of Data.com? Will it be phased out and when? If they are attriting 30% of their revenue this year (a Dun & Bradstreet estimate), how are they guiding their customers to AppExchange solutions in lieu of Data.com?

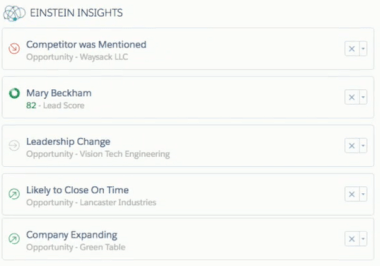

How is Einstein being infused into their Sales Cloud? How are they ensuring that Einstein Insights are based on accurate and timely data?

What is the future of SalesforceIQ CRM technology (it is being decommissioned in 23 months)?

Meeting with Sales and Marketing Intelligence vendors on the floor.

I stopped by several of their sales and platform booths, but nobody had any answers on Data.com. This is the second year in a row in which there was no mention of data or the future of B2B prospecting, data enrichment, or sales intelligence at the event. Salesforce has never been much of a data company. They botched Data.com from Jigsaw acquisition through decommission. A few months after announcing a detailed roadmap at Dreamforce, they cancelled their Dun & Bradstreet content partnership in early 2017.

But if you are going to build analytics into your platform, license the iconic Einstein name for it, and tout it as an enabling technology for all of your clouds, then maybe you should have a strategy for ensuring that Einstein Insights are based upon quality data.

I did get to see a quick demo of Einstein Insights for the Sales Cloud. It provides lead scoring with recommendations so a sales rep can see whether a lead is likely to convert (or other goals) and review the top reasons for the score. It even goes so far as to recommend additional contacts but fails to justify those names. It appeared the names were mined using the SalesforceIQ technology, but all that was demonstrated was the name — no title, level, or reason to reach out to that individual. Salesforce is on the right track here but needs to expand its explanations for lead scores to its contact recommendations.

As to sales and marketing intelligence, there was only one vendor on the floor — Zoominfo. They were demonstrating their new Clean and Complete services for Salesforce. Clean provides batch account, contact, and lead record enrichment while Complete provides account, contact, and lead record appends during data entry and batch upload. Due to the depth of the Zoominfo database, the Complete service has an 80% account match rate and a 65% contact match rate.

Both services support custom mapping. Pricing is based upon record volume.

The keynote lacked the energy of prior years when Keith Block, COO, performed the duties. While Sarah Franklin, EVP of Developer Relations did a fine job, Block is from Boston and made sure the event was localized. Missing this year were sports heroes (e.g. Tom Brady, Bill Belichick) and the Drop Kick Murphys. If you want to wake up a 10:00 AM keynote, the Drop Kicks and their Irish punk are a great way to do so.

I’m a sailor peg

And I’ve lost my leg

Climbing up the top sails

I’ve lost my leg!

I’m shipping up to Boston, whoa…

“I’m Shipping up to Boston,” Drop Kick Murphys

There was a presentation on Year Up (an inner city business training program) with a local success story, but the 75 minutes were basically rehashed Dreamforce partner videos and content with a focus on B2C. Even the B2B example, 21st Century Fox, was equally a promo for “Dead Pool 2” and other Fox properties as it was a demo of Quip and its marketing and project management tools. The distributor relations aspect of the story was a bit light.

So let’s bring back Keith Block next year and expand the exhibition space. The Hynes Exhibitor Floor was too crowded, too hot, and too noisy.

I don’t mean to grouse. Salesforce is a terrific company. They have a strong social mission, a market leading product, and an ability to keep things fun. It’s just that this year didn’t match prior Boston events, and the company has diversified into so many clouds and capabilities that the Sales Cloud and Sales Partner solutions get crowded out.

Dun & Bradstreet’s company profile displayed within their D&B Hoover’s product.

Last week, Dun & Bradstreet CEO Robert Carrigan resigned as CEO, board member, and Chairman. In his absence, Thomas Manning has been appointed Chairman and interim CEO. Manning has been a board member since 2013 and Lead Director since 2016. He previously served as the CEO of Cerberus Asia Operations & Advisory Limited, CEO of Capgemini Asia, and CEO of Ernst & Young Consulting Asia. He was also a senior partner with corporate strategy firm Bain & Company where he led the global IT practice in Silicon Valley and Asia.

No reason was given for Carrigan’s departure beyond that it was a mutual decision.

“Over the last four years we have made progress transforming this company. We’ve improved our data and analytics, developed solutions and capabilities to serve new customer use cases, and modernized our products and platforms. The Board is confident in the strategic direction of the Company, and fully believes that this business can deliver sustainable mid-single digit revenue growth and expanding margins. Our number one priority is accelerating value creation for shareholders.”

Dun & Bradstreet Chairman and interim CEO Thomas Manning

However, the company is not growing revenue and profits quickly enough. To address the slow growth, the firm engaged McKinsey & Company two months ago in a strategic and operational review “to help us find ways to speed up the time to realize value,” said Manning. “The first phase of their work validated our strategy and identified barriers to growth and cost opportunities. The next phase of their work will include a full portfolio and business assessment and we are open to considering all options for value creation that may be identified.”

McKinsey validated the basic DaaS strategy around premium company, contact, and risk data. McKinsey’s primary concern was the “breadth of our offerings and distribution channels” which increased the level of operational complexity. The updated strategy will look to “simplify and streamline the business.”

Dun & Bradstreet is also looking to “apply more specialization to our selling activities as we go deeper into the sales and marketing space,” said Manning. “As we expand our sales and marketing value proposition from being primarily a static data supplier to becoming a dynamic player in the digital sales, marketing and advertising space, we are working to make sure that our organization, go-to-market strategy and processes are aligned with that goal.”

The firm hired David Godfrey, who previously ran Global Sales at Gartner, to oversee go-to-market strategy and execution. He will be reporting into Manning.

James Fernandez, new Lead Director of the Board, said, “As Dun & Bradstreet continues its work to drive sustainable growth, the Board believes now is the right time to transition the Company’s leadership. We are pleased to have a leader of Tom’s caliber and experience to step in as interim CEO. The Board will continue to support the Company, and lend our expertise to the organization and Tom during this transition period as we conduct our search for a permanent successor.”

Q4 Earnings

Q4 earnings increased 3%, but only 1% organically, to $527 million. Total revenue hit $1.75 billion in 2017 with 83% in the Americas. The firm maintained expense discipline resulting in a ten-basis point improvement in margins while investing $40 million on initiatives which “transform our technology platforms in order to meet our customers’ modern-day needs,” said CFO Richard Veldran. “Modernizing delivery of our solutions is a critical component of our strategy.”

Data-as-a-service delivery continues to increase. Nearly 30% of Americas revenue came via as-a-service solutions “which makes our data stickier and more useful for our customers and drives higher-value revenue.”

Amongst the 2017 initiatives were upgrades to D&B Credit and new D&B Optimizer solutions for Salesforce and Microsoft.

Deferred revenue was up 3% year over year before M&A activity and currency adjustments. Growth was attributed to D&B Credit, D&B Hoovers Q4, and the D&B Direct API. President and COO Josh Peirez noted that the D&B Credit Suite revenues were no longer declining and that the company is well-positioned in D&B Credit, D&B Hoovers, and D&B Direct.

“We think we’re well-positioned to address the competitive challenges. We’re also pleased that McKinsey has validated that opportunity and that strategy and helping us to make sure that we are packaging and bundling these things properly.”

Dun & Bradstreet President & COO Josh Peirez

Taxes, which were 31.4% in 2017, are expected to drop to the mid-20s due to the US corporate tax reforms. The reforms will also allow the firm to repatriate $265 million to reduce debt levels.

No guidance was provided as the firm is beginning their operational review. Veldran promised more details on the Q1 call.

Dun & Bradstreet raised its quarterly dividend by two cents to $0.5225 per share.

The market reacted very positively to the announcements, driving Dun & Bradstreet’s stock price up nearly 8% after the earnings call.

Segment Growth

Sales & Marketing Solutions (S&MS) rose 4% in the Americas to $240.1 million in Q4. Growth was led by Sales Acceleration products which rose 9% to $84.3 million. For the full year, Sales Acceleration grew 10% to $288.4 million in the Americas with the Avention acquisition contributing twelve points of growth. Legacy Hoover’s drove down organic Sales Acceleration revenue with traditional Hoovers revenue declining by mid-single digits.

Revenue for the new D&B Hoovers service (Dun & Bradstreet content delivered through the Avention platform) increased in 2017. However, the decline in revenue from the Data.com partnership will result in a decline in 2018 Sales Acceleration revenue. Data.com generated around $50 million in revenue in 2017 with the firm continuing to sell through August 2017, resulting in a flat year. Veldran projects a $15 million decline in Data.com revenue. Dun & Bradstreet is looking to recapture some of that decline as new D&B Hoovers and D&B Optimizer for Salesforce contracts.

Peirez is quite pleased with the trajectory of the D&B Hoovers business. “We think our products are far better than anything else in market. We continue to see the overwhelming majority of customers that are buying our D&B Hoovers product buying the higher level of the product with the integrations to CRM, so that’s extremely encouraging for us.”

The firm is also moving to migrate its Hoover’s customer base over to D&B Hoovers. In Q4, more than ten percent of the legacy base moved to the new platform as Dun & Bradstreet “started to move very aggressively in getting the customers upgraded,” said Peirez. While the D&B Hoovers Suite grew low-single digits in its first year, Peirez expects growth to accelerate in year two. The company has told users that the legacy platform will be phased out at the end of the year.

Advanced Marketing Solutions grew 2% in Q4 to $155.8 million in the Americas. For the full year, growth was 2% to $383.9 million. While revenue was up mid-single digits in H2, the product line was weighed down by H1 weakness.

Outside the Americas, S&MS grew 17% to $16.9 million in Q4. For the year, S&MS non-Americas revenue rose 18% to $60.4 million. Growth was driven by Sales Acceleration products, including the acquired Avention product line. Sales Acceleration products jumped up 24% to $7.5 million in the quarter and 39% to $27.7 million for the year.

The D&B Hoovers Suite rose 26% to $42.6 million in the Americas in Q4 and 22% to $166.5 million. Outside of the Americas, D&B Hoovers Suite rose from $0.6 million to $5.3 million in Q4 and $3.1 million to $16 million. While the classic Hoover’s product line had little overseas sales, the new D&B Hoovers product line, built on the Avention platform, benefited from a longstanding presence in the UK, Singapore, Australia, and India.

Optimizer for Salesforce supports Account Segmentation by Revenue, Employees, Industry, and Location.

For the past nine months, there has been great ambiguity around the future of Data.com, a pair of AppExchange services which combine the old Jigsaw contact file with Dun & Bradstreet account and industry intelligence. Salesforce has remained mum throughout with Dun & Bradstreet providing details on their earnings calls.

Dun & Bradstreet CEO Bob Carrigan announced that Dun & Bradstreet and Salesforce will be offering a path forward for Data.com clients. In August, Salesforce Data.com stopped offering D&B content for new clients, but legacy clients continued to receive D&B WorldBase, Hoovers, and First Research insights. However, the long-term direction of Data.com remained ambiguous as service revenues declined due to “natural attrition.” Carrigan announced that the two firms have agreed on a transition plan to migrate Data.com customers to D&B Hoovers and the new D&B Optimizer for Salesforce.

D&B Hoovers represents a significant upgrade for Data.com Prospector customers as they will receive deeper global company and contact coverage than before. Users will have access to a deeper set of global contacts, a broader set of screening variables, and company intelligence including financials, filings, SWOTs, news, sales triggers, and alerts.

Optimizer for Salesforce will launch next week at Dreamforce where Dun & Bradstreet will have a larger presence than in previous years. Product specifics were not provided on the call, but some details were posted on the AppExchange Lightning Data site. D&B Optimizer offers a data management dashboard, account record matching using DUNSMatch logic across eighty variables, segmentation analysis (revenue, employees, industry and location), family tree linkage opportunities, duplicate record management, and out of business flagging. Updates are made every fifteen days.

D&B Optimizer creates “virtual corporate family trees”

Optimizer for Salesforce is listed at $22 per user per month, $3 less than Data.com Clean. It is currently available in the US and UK.

“For organizations to grow, they need actionable and complete data across the entire business to ensure that timely and informed decisions are being made. D&B Optimizer for Salesforce provides Salesforce customers the ability to get the data they want, when and where they need it, directly within their Salesforce instance. This leads to increased productivity and, ultimately, growth for their businesses.”

Derek Slayton, General Manager of Sales and Marketing LOB, Dun & Bradstreet

Not only will Salesforce assist with transitioning clients, but they will also be referring prospects to Dun & Bradstreet. Dun & Bradstreet will recognize the full revenue from these products and own the customer relationships going forward, providing them with greater control over the product, increased revenue, and an end to their disintermediated status on the AppExchange.

According to Dun & Bradstreet CFO Richard Veldran, Salesforce revenue is “in the neighborhood of $50 million, because they’re not selling new on their side.” In the short term, that revenue will decline due to “natural attrition.” However, as customers are converted to D&B solutions, the firm will no longer be on a revenue share basis with Salesforce, resulting in in a revenue upswing. It should be noted, though, that subscription revenue is ratable over the term of the contract so there will be a delay in this revenue recognition.

But if you are going to build analytics into your platform, license the iconic Einstein name for it, and tout it as an enabling technology for all of your clouds, then maybe you should have a strategy for ensuring that Einstein Insights are based upon quality data.

But if you are going to build analytics into your platform, license the iconic Einstein name for it, and tout it as an enabling technology for all of your clouds, then maybe you should have a strategy for ensuring that Einstein Insights are based upon quality data.